Früher mussten Unternehmen sich in jedem EU-Land separat für die Umsatzsteuer registrieren, sobald sie bestimmte Umsatzgrenzen überschritten.

Seit dem 1. Juli 2021 gibt es eine neue, einheitliche Regelung:

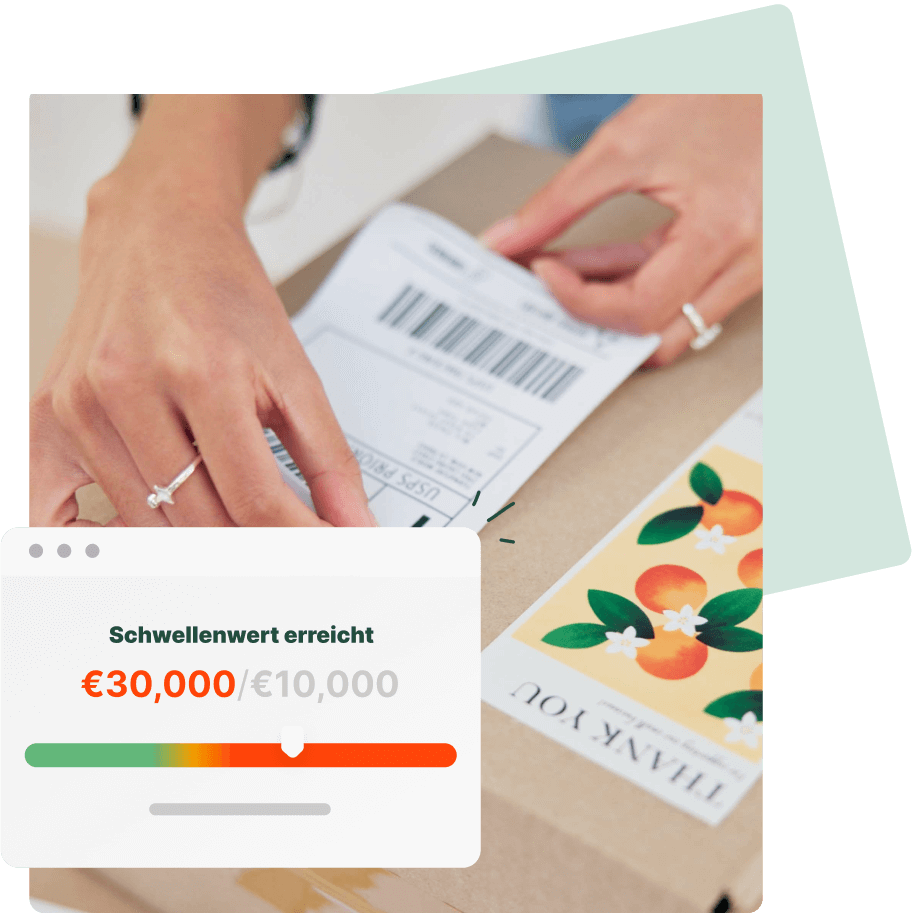

Liegt Dein grenzüberschreitender Umsatz unter 10.000 € pro Jahr, zahlst Du die Umsatzsteuer weiterhin in Deinem eigenen Land.

Sobald Du die 10.000 €-Schwelle überschreitest, kannst Du Dich über den

One-Stop-Shop (OSS) zentral registrieren – und Deine Umsatzsteuer für alle EU-Verkäufe bequem über eine einzige Meldung abführen. Mehr Informationen hat die

Europäische Kommission zusammen gestellt.

Kurz zusammengefasst:

.png)